Punggol vs Sengkang Q1 2026: Two Towns, One Price Band, Very Different Markets

Summary

Punggol and Sengkang's average resale prices are virtually identical in Q1 2026, but the data reveals a tale of two markets — Sengkang offers price consistency, while Punggol offers a high-end ceiling driven by rare loft-format stock along Punggol Drive.

Across January, February, and March 2026, Sengkang recorded 423 transactions at a weighted average price of S$676,854, while Punggol logged 403 transactions at S$672,537 — a gap of just S$4,317, or roughly 0.6 percent. That's statistical noise. In effect, the two towns trade at the same price. Yet the distribution behind that average looks quite different.

A note on methodology: town-level averages reflect the mix of flat types transacted in any given quarter. Both Punggol and Sengkang skew heavily toward 4-room and 5-room flats reflecting their relatively young housing stock, so the comparison here is close to apples-to-apples. Readers evaluating a specific flat type should still check flat-type-level pricing.

Punggol vs Sengkang at a Glance

| Town | Q1 Transactions | Weighted Avg Price | Highest Q1 Deal |

|---|---|---|---|

| Sengkang | 423 | S$676,854 | S$1,128,888 |

| Punggol | 403 | S$672,537 | S$1,470,000 |

The Price Twin, the Volume Twin

Sengkang and Punggol transacted almost identical volumes in Q1 2026 — 423 vs 403 flats — at almost identical average prices. Both towns are dominated by post-2000 housing stock, both are LRT-served, and both feed buyers onto the same NEL spine toward Dhoby Ghaut and HarbourFront.

For a buyer comparing the two on financial terms alone, the answer is: it doesn't matter. A S$4,000 gap on a flat this size is lost in renovation contingency.

Where the two towns diverge is at the top of the market.

The Streets Behind the Ceiling

When you look at which specific blocks drove each town's top deals, the divergence sharpens considerably. Aggregate averages hide what's happening at the street level — so here's where the premium money actually landed in Q1 2026.

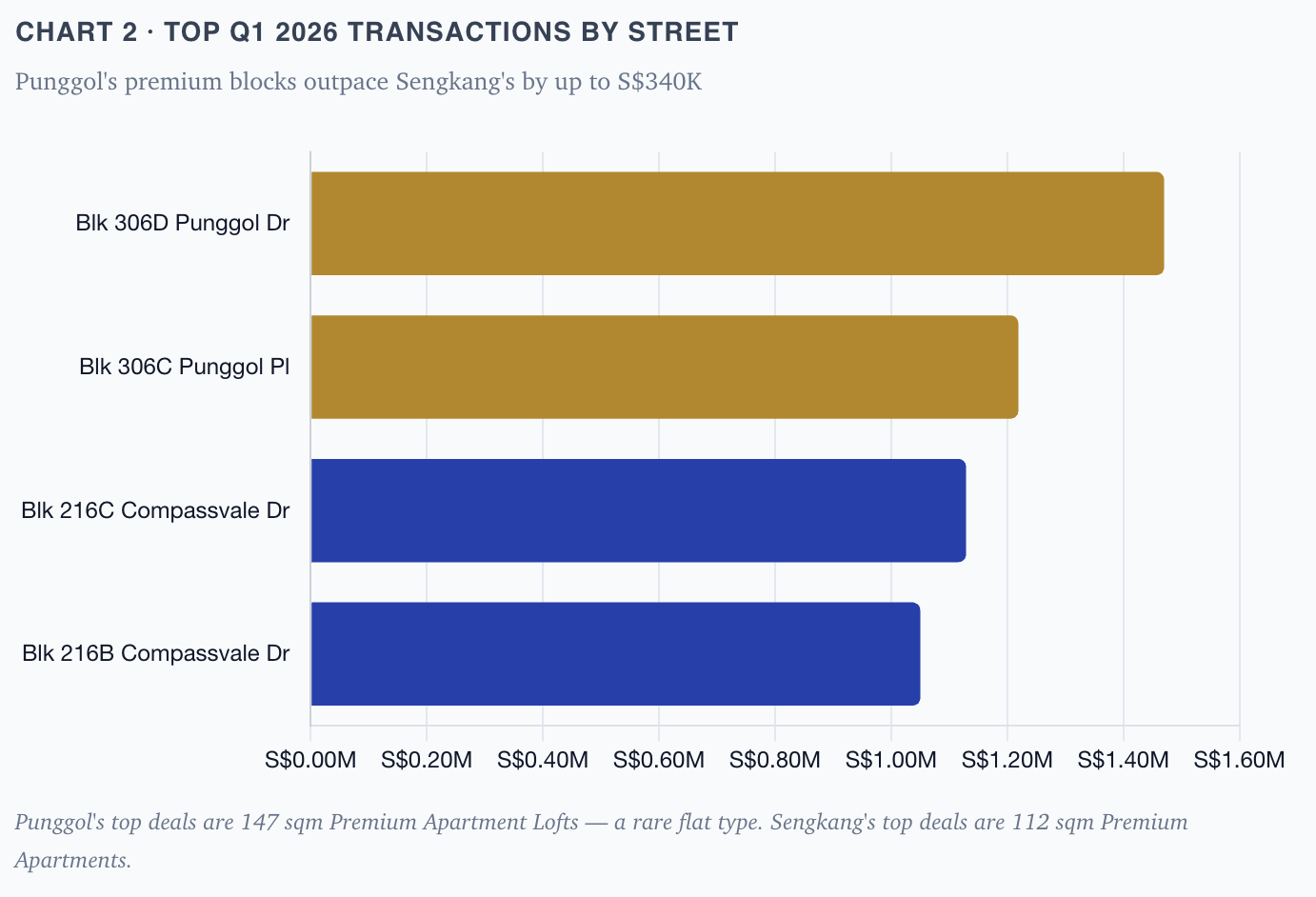

Punggol — premium streets

| Block / Street | Flat Type | Floor | Area | Price |

|---|---|---|---|---|

| Blk 306D Punggol Drive | 5 Room Premium Apt Loft | 16–18 | 147 sqm | S$1,470,000 |

| Blk 306C Punggol Place | 5 Room Premium Apt Loft | 16–18 | 147 sqm | S$1,218,888 |

Both of Punggol's top Q1 deals came from essentially the same block cluster — Blk 306C and 306D along Punggol Drive / Punggol Place. These are Premium Apartment Loft units at 147 sqm, materially larger than a typical 5-room (110–120 sqm), with high ceilings and a dual-storey layout. The blocks sit within the Punggol Waterway vicinity, close to Waterway Point and the Punggol MRT/LRT interchange.

Why these streets command the premium:

- Loft configuration rarity. Premium Apartment Loft is a relatively scarce flat type — the dual-level layout and 140+ sqm footprint position these units against condo alternatives rather than typical HDB stock.

- Waterway and interchange proximity. Blk 306-series sits within walking distance of Punggol Waterway Park, Waterway Point mall, and the Punggol MRT/LRT interchange. This is as close to "mature estate convenience" as Punggol gets.

- Unblocked outlook. Units on the 16–18 floor band benefit from open views over low-rise civic land and water features to the north.

Sengkang — premium streets

| Block / Street | Flat Type | Floor | Area | Price |

|---|---|---|---|---|

| Blk 216C Compassvale Drive | 5 Room Premium Apt | 16–18 | 112 sqm | S$1,128,888 |

| Blk 216B Compassvale Drive | 5 Room Premium Apt | 13–15 | 112 sqm | S$1,050,000 |

Sengkang's two highest 5-room Q1 deals both came from Compassvale Drive (Blk 216B and 216C) — Premium Apartment units at a more standard 112 sqm. Compassvale sits within the Sengkang Town Centre cluster, close to Compass One mall and Sengkang MRT/LRT.

Why Compassvale leads Sengkang:

- Town-centre location. Blk 216-series is within the most central cluster of Sengkang, immediately adjacent to Compass One and the MRT interchange — Sengkang's equivalent of Punggol's Waterway Point catchment.

- Relatively newer stock. With 90+ years remaining lease, these units are well within the CPF-fundable and full-LTV envelope for younger buyers.

- Premium Apartment layout. A step up from standard Model A 5-rooms, but notably not loft configuration — and this is where Sengkang's ceiling is structurally capped.

Where the lower-priced transactions sit

At the other end of the price range, both towns have pockets consistently transacting below their town average:

Punggol's softer pockets tend to be blocks further from Punggol MRT/LRT and away from the Waterway — particularly the eastern reach toward Punggol Coast before the Cross Island Line delivers improved connectivity. 4-room flats in these outer blocks transact notably below the town average, driven by longer bus-to-MRT journeys and less immediate amenity access.

Sengkang's softer pockets tend to sit on the LRT loop segments furthest from the main Sengkang MRT station — Fernvale, Kupang, and Thanggam in particular. Buyers face an LRT-then-MRT commute rather than a direct MRT trip, and amenity density drops off noticeably beyond the central cluster.

In both cases, the pattern is the same: proximity to the main MRT/LRT interchange and the town centre mall drives a premium of roughly S$50K–S$150K over comparable flats on the outer reaches of the LRT loop.

What the Street Data Tells Us

The headline numbers said Punggol and Sengkang are near-twins. The street-level data tells a subtly different story:

- Same average, different dispersion. While the two towns' average prices are virtually identical, Punggol exhibits significantly higher price dispersion — its top deals pull further from its median than Sengkang's do. This partly reflects development history: Sengkang was built largely as a consolidated series of HDB residential clusters, producing a more homogenous housing stock. Punggol was developed in more distinct phases — from the older central clusters to the newer, architecturally distinct Waterway-facing projects — so it naturally carries wider valuation variance.

- Punggol's ceiling is driven by a scarce flat type (147 sqm Loft) in a specific block cluster. Remove Blk 306C/D from the picture and Punggol's top deal would sit closer to Sengkang's S$1.13M ceiling.

- Sengkang's premium segment is more uniform. Its top deals are in standard-configuration Premium Apartments, meaning Sengkang's entire 5-room market behaves more consistently.

- The floor — the lower-priced pockets — follows the same structural rule in both towns. Distance from the main interchange and town centre mall is the single strongest driver of discount.

This matters for buyers because it means the "Punggol premium" is not a town-wide phenomenon — it is concentrated in a handful of large-format, waterway-adjacent loft units. If you're shopping for a standard 5-room in Punggol vs Sengkang, the two markets genuinely do trade at the same price, and your decision should come down to which town centre and MRT access suits your life better.

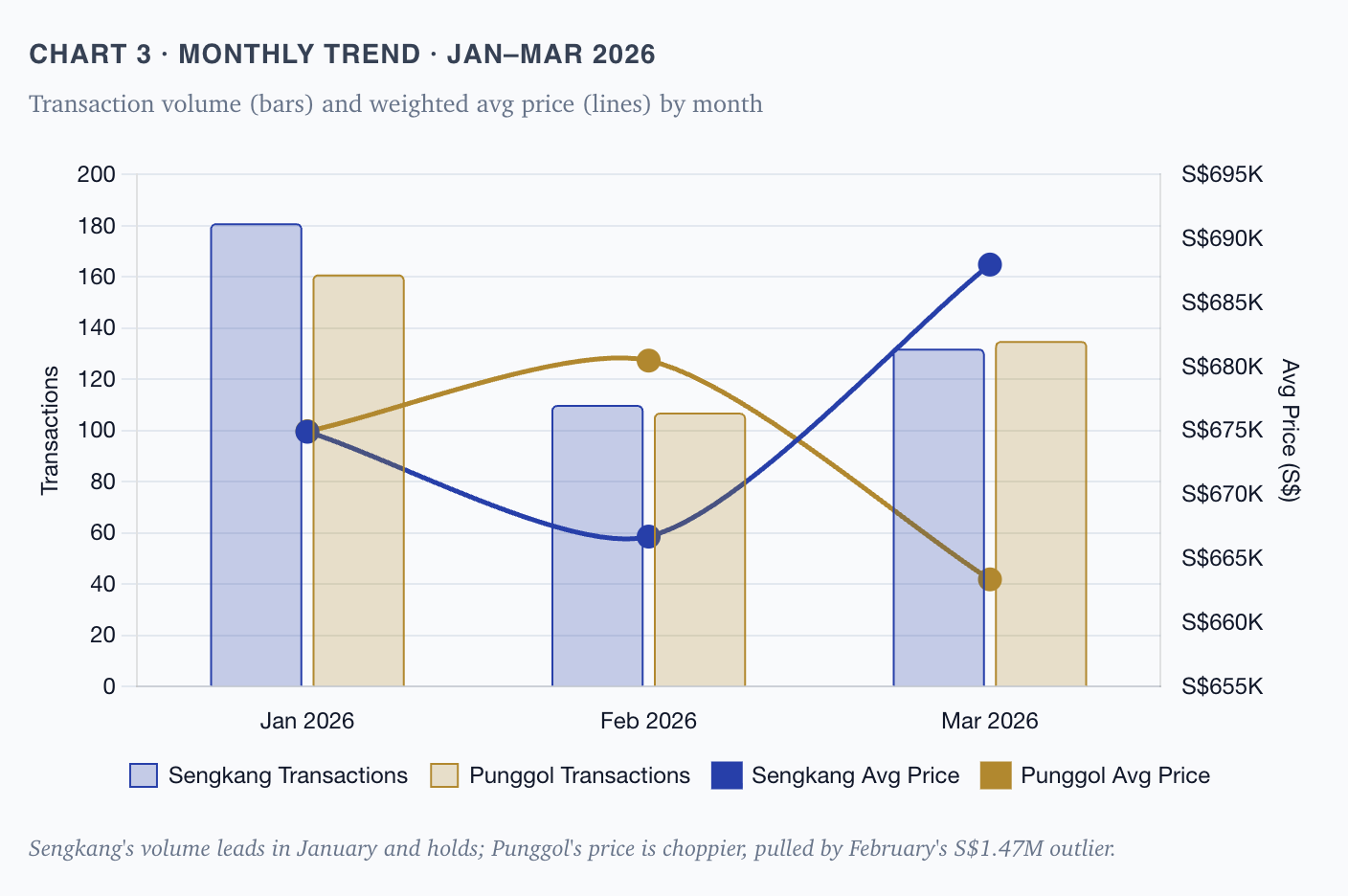

Volume Patterns: A Steady Sengkang, a Front-Loaded Punggol

Looking month by month, the two towns show different quarterly rhythms.

Sengkang's volume leads in January and holds through the quarter with a modest price lift in March (+1.9% vs January). Punggol's pattern is choppier — average price rose in February (partly boosted by that S$1.47M outlier) and then retraced in March. For sellers, the takeaway is that Sengkang's market is slightly more predictable on a month-to-month basis, while Punggol's monthly averages are more sensitive to individual high-end transactions moving through the mix.

Looking month by month, the two towns show different quarterly rhythms.

Forward Look

There is little structural reason for this Sengkang-Punggol price convergence to break in the near term — both towns share similar vintage, connectivity, and flat-type mix. The most plausible medium-term disruptor is the Cross Island Line — Punggol Extension, currently under construction and targeted for completion in 2032. Once operational, it will link Punggol directly to Pasir Ris (and onward to the main CRL spine), materially improving east-west connectivity for Punggol. This is a prospective, not imminent, shift — buyers in Q1 2026 are not yet pricing it in meaningfully.

Both towns also sit within Singapore's broader decentralisation push. Punggol Digital District is entering its operational phase in 2026, but it is not yet a mature employment hub comparable to the CBD or Jurong Lake District. Its effect on housing demand remains prospective rather than historically established, which is why current resale pricing in both towns stays anchored to residential fundamentals — flat type, lease, MRT access — rather than workplace-proximate premiums.

The gap worth watching is not the overall town average but the ceiling deals. If Punggol Drive / Punggol Place loft transactions continue printing at S$1.3M–1.5M while Compassvale Drive tops out at S$1.1M, Punggol will increasingly be perceived as the "premium" North-East town even though the bulk of its stock trades identically to Sengkang. The more informative metric in H2 2026 will be each town's top decile price, not the average.

What This Means for Buyers

A quick decision framework based on the Q1 2026 data:

- Shopping a standard 4-room or 5-room? Treat Punggol and Sengkang as interchangeable on price. Pick based on which town centre you prefer (Waterway Point vs Compass One), which LRT stop suits your commute, and school catchment.

- Targeting S$1.2M+ premium stock? Punggol's Blk 306-series loft units offer something Sengkang doesn't replicate. Sengkang's premium segment tops out around S$1.13M on standard-format Premium Apartments.

- Budget-constrained? In either town, prioritise proximity to the main MRT interchange over the town name itself. Fringe LRT blocks — Fernvale/Kupang/Thanggam in Sengkang, outer Punggol Coast in Punggol — transact at notable discounts, but the commute and amenity trade-offs are real.

- Selling? Sengkang offers slightly more predictable exit pricing; Punggol offers more upside variance if your unit happens to be large-format or waterway-adjacent.

The Takeaway

Punggol and Sengkang are, on the numbers, a draw. Average prices differ by less than 1 percent, volumes are within 5 percent of each other, and both towns represent the modern North-East lifestyle product at the same price point.

The interesting divergence is at the ceiling — and the street data reveals what drives it. Punggol's Blk 306C/306D on Punggol Drive and Punggol Place produced loft-format 147 sqm units that transacted at S$1.22–1.47M, well above Sengkang's top deals on Compassvale Drive (Blk 216B/216C) at S$1.05–1.13M. This is not a general Punggol premium — it's a specific-stock, specific-street phenomenon.

At the average, Punggol and Sengkang are interchangeable. At the extremes, they are not. And for most buyers, it's the street — not the town — that determines value.

Methodology & Data Source

- Source: Kriosm analysis of HDB resale transaction data (data.gov.sg), Q1 2026.

- Period covered: January–March 2026 (transaction registration date).

- Averaging method: Quarterly figures are volume-weighted across the three months — Σ(monthly transactions × monthly avg price) ÷ Σ(monthly transactions).

- Scope: All HDB resale flat types (1-room through Executive). No filtering applied by flat model, floor area, or lease band.

- Caveat on the weighted average: This approach smooths monthly volatility, but does not correct for shifts in the mix of flat types transacting in any given month. Readers should treat the headline figures as town-level trend indicators, not as a precise price-per-square-metre gauge.