June 2026 BTO Launch: 6,952 Flats Across 7 Projects, Three Tiers, One New Estate

Summary

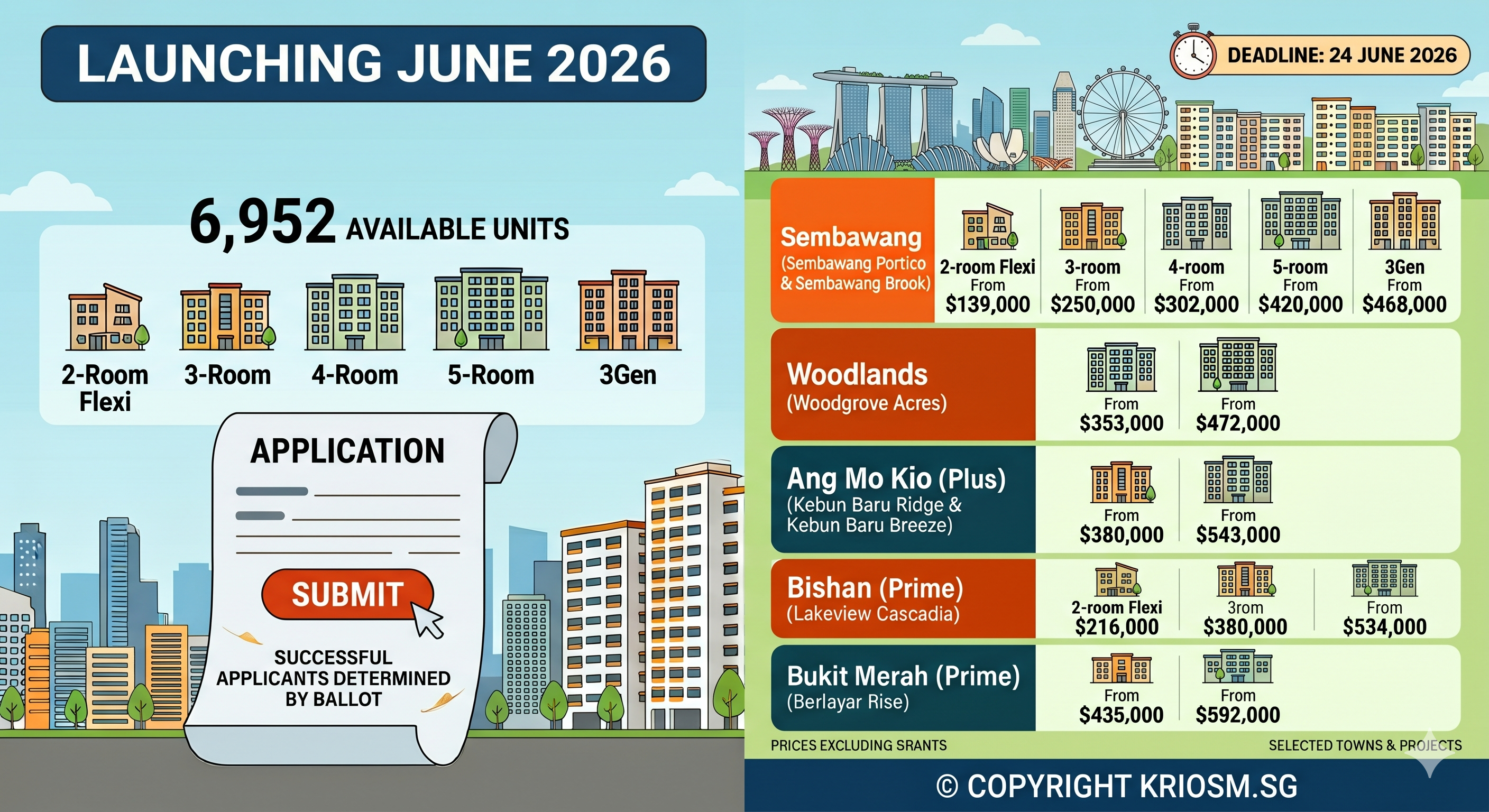

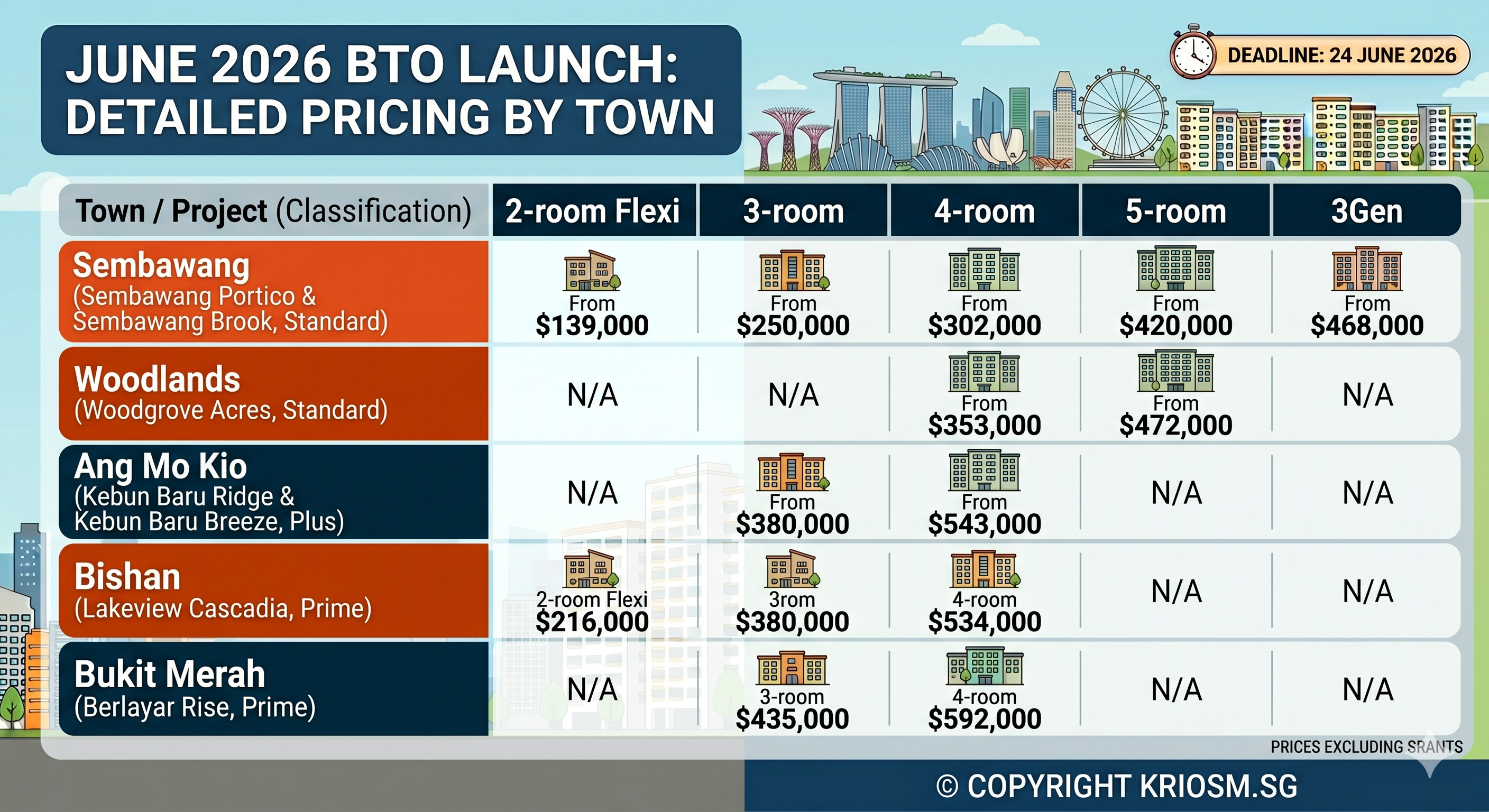

HDB opened applications today for the June 2026 Build-To-Order exercise, offering 6,952 flats across seven projects in Sembawang, Woodlands, Ang Mo Kio, Bishan, and Bukit Merah. Applications close 24 June 2026, 11:59pm, with successful applicants determined by computer ballot rather than first-come-first-served. This launch is notable for spanning all three of HDB's classification tiers — Standard, Plus, and Prime — in a single exercise, giving buyers a rare side-by-side comparison of how each tier is priced.

The three-tier spread, in one launch

This exercise puts Standard, Plus, and Prime projects on the table at the same time, and the pricing gap between tiers is stark.

At the Standard end, Woodgrove Acres in Woodlands offers 2-room Flexi units from $137,000 before grants, with 4-room flats starting at $353,000. Sembawang's twin projects, Sembawang Portico and Sembawang Brook, price similarly — 4-room flats from $302,000, and the rare 3Gen flat type from $468,000.

Move to the Plus tier and the picture shifts. Kebun Baru Ridge and Kebun Baru Breeze in Ang Mo Kio price 4-room flats from $543,000 — roughly 80% above the Woodlands equivalent — reflecting the tighter subsidy recovery and stricter resale conditions that come with Plus classification in a mature, central-fringe town.

At the top, Prime-tier Berlayar Rise in Bukit Merah prices 4-room flats from $592,000 before grants, the highest 4-room starting price in this exercise. Lakeview Cascadia in Bishan, also Prime, skips the 3-room and 5-room categories entirely, offering only 2-room Flexi (from $216,000) and 4-room (from $534,000) — a flat-type mix that signals HDB is positioning this project primarily for young couples and small families rather than multi-generational households.

What this means for the data: the within-launch spread between Standard and Prime 4-room pricing — roughly $290,000 at the floor — is one of the widest seen in a single BTO exercise. As these cohorts clear their MOP in 5+ years, expect the resale market to inherit this same stratification, with Plus and Prime-tier resale flats commanding premiums tied not just to location but to the subsidy clawback structure baked into their tier.

Grants narrow the gap, but not by the same margin everywhere

The grant-inclusive pricing tells a different story than headline prices alone. A 2-room Flexi flat at Berlayar Rise drops from $247,000 to $127,000 after grants — roughly a 49% reduction. The same flat type at Woodgrove Acres drops from $137,000 to just $17,000, an ~87.6% reduction. First-timer households at the lower end of the income ladder are clearly being steered toward Standard-tier, non-mature estate options, where grants do dramatically more work relative to the headline price.

What this means for the data: when comparing "affordability" across towns using only excluding-grants prices, the real picture for first-timer buyers is understated for Standard-tier projects and overstated for Prime-tier ones. Any analysis on Kriosm comparing BTO affordability by town should flag both price columns, not just one.

One project, two names — and what that signals

Sembawang's allocation is split across two project names, Sembawang Portico and Sembawang Brook, both Standard tier, both offering the full range from 2-room Flexi through 3Gen flats. Pairing two project names under one town allocation at the same tier is typically how HDB manages larger combined launches without inflating a single project to an unwieldy unit count — worth noting if you're tracking project-level versus town-level supply in Sembawang going forward.

What to watch on Kriosm

- 4-room resale prices in Woodlands and Sembawang over the next 5 years, as this Standard-tier cohort's MOP clock starts running from today's application

- Ang Mo Kio's Plus-tier resale ceiling once Kebun Baru Ridge and Kebun Baru Breeze clear MOP — Plus tier comes with a longer MOP and tighter resale eligibility, which should keep early resale volume lower than a Standard-tier launch of similar size

- Bishan's Lakeview Cascadia as a price benchmark once it reaches resale — given the unusual 2-room/4-room-only mix, its resale comparables may need to be drawn from Bishan's existing private and HDB stock rather than other BTO cohorts

- Application rates on the HDB Flat Portal during the 17–24 June window as an early demand signal, particularly the gap between Berlayar Rise (Prime, Bukit Merah) and Woodgrove Acres (Standard, Woodlands) — the widest price-tier contrast in this exercise